The 2026 Global Mortgage Landscape: Why Spain Leads the Way

As we move through the first quarter of 2026, the international real estate market is witnessing a fascinating divergence in financing costs. For the global investor, the "cost of debt" has become the primary metric for determining where to park capital. While traditional powerhouses like London and New York continue to grapple with high-interest environments and complex tax structures, the Spanish mortgage market—specifically for non-residents—has emerged as a beacon of stability and competitive value.

The Spanish Advantage: 2026 Interest Rate Realities

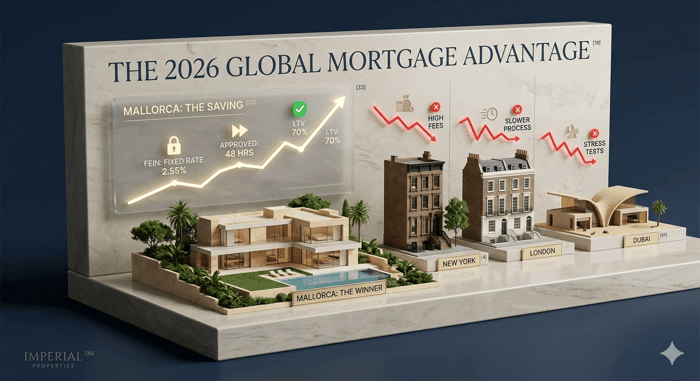

In early 2026, the European Central Bank's monetary policy has led to a stabilization of the Euribor, which currently hovers around 2.25%. For non-resident buyers in Mallorca, this translates to incredibly attractive borrowing terms compared to other global hubs. While mortgage rates in the United States are still frequently quoted above 6.5%, and the UK market sees average fixed rates for premium properties sitting between 4.5% and 4.8%, Spanish banks are offering non-residents fixed rates starting as low as 2.55% for high-profile applicants. Even standard non-resident products are comfortably sitting in the 3.2% to 3.8% range.

This "interest rate gap" is driving a surge in American and British buyers who realize that their purchasing power is effectively 30% higher in the Balearics than in their home markets when financing is considered. A €2 million villa in Nova Santa Ponsa, financed at 70% LTV, currently carries a significantly lower monthly debt service than a comparable property in the Hamptons or the Surrey hills.

LTV and the "LCCI" Protection

One of the most significant changes for 2026 is the maturity of the Spanish Mortgage Law (LCCI). This legislation has made the Spanish market one of the most transparent in the world. Every non-resident borrower now receives a FEIN (European Standardised Information Sheet), which is a legally binding offer that the bank cannot change for 10 days. Furthermore, the mandatory "Acta Previa" appointment with a Spanish notary ensures that every buyer fully understands their contract before signing. For international investors used to the often opaque "fine print" of other jurisdictions, this level of consumer protection is a massive confidence booster.

In terms of Loan-to-Value (LTV), 2026 standards have remained firm. Non-residents can typically secure 60% to 70% financing. While residents can occasionally reach 80%, the 70% ceiling for overseas buyers acts as a built-in safety mechanism, ensuring that the local market remains resilient and free from the sub-prime risks seen in other global regions.

Comparing the Competitors: New York, London, and Dubai

When we look at the competition, the choice for 2026 becomes clear. In New York, despite a slight cooling of rates, the total "closing costs" and ongoing property taxes often double the effective cost of ownership. In London, while the Bank of England base rate has eased to 3.75% as of February 2026, the stress-testing for luxury mortgages remains incredibly stringent, often limiting borrowing capacity for those with complex international income streams. Dubai, while offering a tax-free environment, often requires much higher deposits for foreigners—frequently up to 50%—and utilizes a mortgage structure that offers far less long-term rate certainty than the Spanish fixed-rate models.

Market FAQ: 2026 Edition

Can a US citizen get a mortgage in Spain in 2026?

Absolutely. US citizens are currently among the most active non-resident borrowers. While Spanish banks don't use FICO scores, they accept US tax returns (1040s) and credit reports to verify stability. LTV is generally capped at 70%.

What is the maximum age for a Spanish mortgage?

In 2026, most lenders require the mortgage to be paid off by the age of 75. For a 60-year-old buyer, this would typically limit the term to 15 years.

Do I need to be in Spain to sign my mortgage?

Not necessarily. While the "Acta Previa" and the final deed signature require a notary, these can often be handled via a Power of Attorney (Escritura de Poder) granted to your lawyer.

El Panorama Hipotecario Global 2026: Por qué España Lidera el Camino

A medida que avanzamos por el primer trimestre de 2026, el mercado inmobiliario internacional es testigo de una fascinante divergencia en los costes de financiación. Para el inversor global, el "coste de la deuda" se ha convertido en la métrica principal para determinar dónde colocar el capital. Mientras que las potencias tradicionales como Londres y Nueva York siguen lidiando con entornos de tipos altos y estructuras fiscales complejas, el mercado hipotecario español —específicamente para no residentes— ha surgido como un faro de estabilidad y valor competitivo.

La Ventaja Española: Realidades de los Tipos de Interés en 2026

A principios de 2026, la política monetaria del Banco Central Europeo ha llevado a una estabilización del Euríbor, que actualmente ronda el 2,25%. Para los compradores no residentes en Mallorca, esto se traduce en condiciones de préstamo increíblemente atractivas en comparación con otros centros globales. Mientras que los tipos hipotecarios en los Estados Unidos todavía se sitúan frecuentemente por encima del 6,5%, y el mercado del Reino Unido ve tipos fijos medios para propiedades premium de entre el 4,5% y el 4,8%, los bancos españoles están ofreciendo a los no residentes tipos fijos desde tan solo el 2,55% para perfiles solventes. Incluso los productos estándar para no residentes se sitúan cómodamente en el rango del 3,2% al 3,8%.

Esta "brecha de tipos de interés" está impulsando un aumento de compradores estadounidenses y británicos que se dan cuenta de que su poder adquisitivo es efectivamente un 30% mayor en Baleares que en sus mercados de origen cuando se considera la financiación. Una villa de 2 millones de euros en Nova Santa Ponça, financiada con un 70% de LTV, conlleva actualmente un servicio de deuda mensual significativamente menor que una propiedad comparable en los Hamptons o en las colinas de Surrey.

LTV y la Protección de la "LCCI"

Uno de los cambios más significativos para 2026 es la madurez de la Ley de Contratos de Crédito Inmobiliario (LCCI). Esta legislación ha convertido al mercado español en uno de los más transparentes del mundo. Todo prestatario no residente recibe ahora una FEIN (Ficha Europea de Información Normalizada), que es una oferta legalmente vinculante que el banco no puede cambiar durante 10 días. Además, la cita obligatoria del "Acta Previa" con un notario español asegura que cada comprador comprenda plenamente su contrato antes de firmar. Para los inversores internacionales acostumbrados a la "letra pequeña" a menudo opaca de otras jurisdicciones, este nivel de protección al consumidor es un gran generador de confianza.

Comparando competidores: Nueva York, Londres y Dubái

Al observar la competencia, la elección para 2026 es clara. En Nueva York, a pesar de un ligero enfriamiento de los tipos, los costes de cierre y los impuestos sobre la propiedad a menudo duplican el coste efectivo de propiedad. En Londres, aunque el tipo base del Banco de Inglaterra ha bajado al 3,75% en febrero de 2026, las pruebas de esfuerzo para hipotecas de lujo siguen siendo increíblemente estrictas. Dubái, aunque ofrece un entorno libre de impuestos, a menudo requiere depósitos mucho más altos para los extranjeros —frecuentemente hasta el 50%— y utiliza una estructura hipotecaria que ofrece mucha menos certeza de tipos a largo plazo que los modelos españoles de tipo fijo.

Preguntas Frecuentes del Mercado: Edición 2026

¿Puede un ciudadano estadounidense obtener una hipoteca en España en 2026?

Absolutamente. Los ciudadanos estadounidenses se encuentran actualmente entre los prestatarios no residentes más activos. Los bancos españoles aceptan declaraciones de impuestos de EE. UU. (1040) y informes de crédito para verificar la estabilidad.

¿Cuál es la edad máxima para una hipoteca española?

En 2026, la mayoría de los prestamistas exigen que la hipoteca esté pagada a la edad de 75 años.

Die globale Hypothekenlandschaft 2026: Warum Spanien führend ist

Im ersten Quartal 2026 erlebt der internationale Immobilienmarkt eine faszinierende Divergenz bei den Finanzierungskosten. Für den globalen Investor sind die "Schuldenkosten" zur wichtigsten Kennzahl für die Kapitalanlage geworden. Während traditionelle Märkte wie London und New York weiterhin mit Hochzinsumfeldern zu kämpfen haben, hat sich der spanische Hypothekenmarkt — insbesondere für Nicht-Residenten — als ein Hort der Stabilität und des Wettbewerbsvorteils erwiesen.

Der Spanien-Vorteil: Zinsrealitäten im Jahr 2026

Anfang 2026 hat die Geldpolitik der Europäischen Zentralbank zu einer Stabilisierung des Euribor geführt, der derzeit bei etwa 2,25 % liegt. Für nicht-residente Käufer auf Mallorca bedeutet dies unglaublich attraktive Kreditkonditionen im Vergleich zu anderen globalen Zentren. Während Hypothekenzinsen in den USA häufig noch über 6,5 % liegen und der britische Markt durchschnittliche Festzinssätze für Premium-Immobilien zwischen 4,5 % und 4,8 % verzeichnet, bieten spanische Banken Nicht-Residenten Festzinssätze ab 2,55 % an. Sogar Standardprodukte für Nicht-Residenten liegen komfortabel im Bereich von 3,2 % bis 3,8 %.

LTV und der Schutz durch das "LCCI"-Gesetz

Eine der bedeutendsten Entwicklungen für 2026 ist die Etablierung des spanischen Hypothekengesetzes (LCCI). Diese Gesetzgebung hat den spanischen Markt zu einem der transparentesten der Welt gemacht. Jeder nicht-residente Kreditnehmer erhält nun ein FEIN (Europäisches Standardisiertes Informationsblatt), ein rechtsverbindliches Angebot, das die Bank 10 Tage lang nicht ändern darf. Zudem stellt der obligatorische Termin zur "Acta Previa" bei einem spanischen Notar sicher, dass jeder Käufer seinen Vertrag vor der Unterzeichnung vollständig versteht.

Wettbewerbsvergleich: New York, London und Dubai

In New York verdoppeln Abschlusskosten und laufende Grundsteuern oft die effektiven Kosten. In London sind die Stresstests für Luxushypotheken nach wie vor unglaublich streng. Dubai bietet zwar ein steuerfreies Umfeld, verlangt aber oft viel höhere Anzahlungen von Ausländern — häufig bis zu 50 % — und nutzt Strukturen, die weniger langfristige Zinssicherheit bieten als die spanischen Festzinsmodelle.

Markt-FAQ: Ausgabe 2026

Können US-Bürger 2026 in Spanien eine Hypothek aufnehmen?

Ja, US-Bürger gehören derzeit zu den aktivsten nicht-residenten Kreditnehmern. Spanische Banken akzeptieren US-Steuererklärungen (1040s) zur Prüfung der Bonität.

Was ist das Höchstalter für eine spanische Hypothek?

Im Jahr 2026 verlangen die meisten Kreditgeber, dass die Hypothek bis zum Alter von 75 Jahren getilgt ist.