Table of Contents

- The 3 Percent Retention — What It Is and Why It Exists

- Capital Gains Tax — The Rates and How the Gain Is Calculated

- British Sellers Post-Brexit and the UK-Spain Double Tax Treaty

- Plusvalía Municipal — The Tax That Catches People Out

- Making Sure Your IRNR Declarations Are Up to Date Before You Sell

- The Energy Performance Certificate — A Legal Requirement Before Listing

- The Full Cost of Selling — What Comes Out of the Sale Price

- The Timeline — From Decision to Completion

- FAQs

Selling Property in Mallorca as a Non-Resident: Tax, Process and What Most People Get Wrong

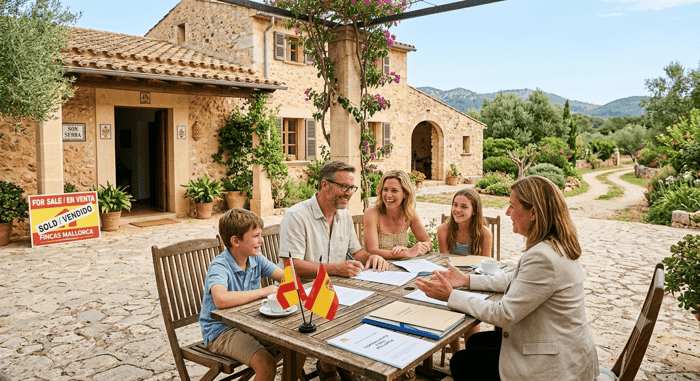

Selling a property in Mallorca as a non-resident is a more straightforward process than most owners expect — but it contains a handful of specific requirements and tax mechanics that differ enough from the process in the UK, Germany, Scandinavia and other common seller home countries to catch people out. The most common mistakes are not dramatic ones. They are things like not having the non-resident income tax declarations up to date before attempting to sell, not understanding what the 3 percent retention actually is and how to get it back if you have overpaid, confusing the plusvalía municipal with the capital gains tax, and not knowing that the energy performance certificate is now a legal requirement before the property can be listed. None of these are insurmountable obstacles — but all of them are significantly easier to manage if you understand them before you start the process rather than discovering them halfway through it. This guide covers the complete picture: the taxes, the process, the costs, the timeline and the specific rules that apply to non-resident sellers in Mallorca in 2026.

The 3 Percent Retention — What It Is and Why It Exists

The single most distinctive feature of selling a Spanish property as a non-resident is the 3 percent retention. When a non-resident sells a property in Spain, the buyer is legally required to withhold 3 percent of the agreed purchase price and pay it directly to the Spanish tax authority (Agencia Tributaria, AEAT) within one month of completion. This is not a tax in itself — it is a prepayment against the seller's capital gains tax liability, held by the state as security because a non-resident seller could, in theory, receive the full purchase price and leave the country without paying any capital gains tax at all.

The 3 percent is calculated on the full gross purchase price, not on the gain. On a 1 million euro sale, the buyer retains 30,000 euros and pays it to the AEAT on the seller's behalf via Modelo 211. The seller receives the net purchase price — in this case, 970,000 euros — at the notary signing.

The retention is not the tax itself, and this is where many sellers are confused. If the seller's actual capital gains tax liability is less than 30,000 euros — which is common for sellers who bought many years ago at a much lower price and have a substantial gain that, after the deductible costs, results in a tax bill below the 3 percent retention — the seller can file a reclamation claim to recover the difference. If the actual CGT liability is higher than the 3 percent retention, the seller must pay the additional amount to the AEAT. The reclamation is filed via Modelo 210 within three months of the sale completing and the 211 being filed by the buyer. The AEAT typically takes 6 to 18 months to process refunds, and the application must be managed by the seller's Spanish tax representative or lawyer since non-residents are required to have a fiscal representative in Spain for this process.

Capital Gains Tax — The Rates and How the Gain Is Calculated

Non-resident sellers pay capital gains tax in Spain under the IRNR (Impuesto sobre la Renta de No Residentes) at a flat rate of 19 percent on the net capital gain. This 19 percent rate applies to both EU and EEA sellers and — since the 2015 reform that equalised rates — to non-EU sellers including British nationals post-Brexit. The historic 21 to 24 percent rates that previously applied to non-EU sellers are no longer in force; the rate is uniformly 19 percent regardless of the seller's nationality.

The capital gain is calculated as the difference between the net selling price and the net acquisition cost. The net selling price is the agreed sale price minus the verifiable costs of selling — the agent's commission, the notary fees attributable to the seller, the seller's lawyer's fees and the plusvalía municipal tax paid. The net acquisition cost is the original purchase price plus the purchase costs paid at the time of buying (ITP or VAT, notary fees, lawyer's fees, land registry fees paid by the buyer) plus the cost of any capital improvements made to the property during ownership, provided those improvements are properly documented with invoices and building licences. Routine maintenance costs — repainting, garden upkeep, minor repairs — are not deductible. Capital improvements — a new pool, a full kitchen renovation with building licence, an extension — are deductible if properly evidenced.

The practical implication of this calculation is that sellers who have owned their Mallorca property for many years and who have carried out significant documented improvements during ownership will often find their taxable gain considerably lower than the gross difference between their purchase price and their sale price. Engaging a Spanish tax adviser to model the gain before finalising the sale price is always worthwhile — the calculation can produce surprises in both directions.

British Sellers Post-Brexit and the UK-Spain Double Tax Treaty

British nationals selling a Mallorca property in 2026 pay the same 19 percent CGT rate as any other non-EU seller. The UK-Spain Double Tax Agreement (DTA), which remains fully in force post-Brexit, gives Spain primary taxing rights over gains arising from the disposal of Spanish property. The DTA provides a credit mechanism that prevents double taxation — British sellers declare the Spanish capital gain to HMRC and receive a credit for the Spanish tax paid, meaning the UK does not tax the same gain twice. The specific interaction between Spanish CGT and UK CGT (which has its own rates and annual exemption) depends on the individual's full tax position and requires advice from a tax professional familiar with both regimes.

Plusvalía Municipal — The Tax That Catches People Out

The plusvalía municipal — formally the Impuesto sobre el Incremento de Valor de los Terrenos de Naturaleza Urbana — is a local municipal tax on the increase in the cadastral value of the urban land element of a property during the period of ownership. It is separate from the capital gains tax and is payable to the local municipality (in Santa Ponsa and the southwest, this is the Calvià Ajuntament) within 30 days of the sale completing.

The plusvalía is calculated on the cadastral value of the land (not the total property value, and not the market sale price) and the number of years of ownership, using coefficients set by the municipality each year. On a property held for ten years in the Calvià municipality, the plusvalía bill typically runs between 3,000 and 15,000 euros depending on the cadastral value of the land. It is conventionally paid by the seller, though the parties can agree otherwise contractually — but in Mallorca market practice, sellers pay it.

The plusvalía was the subject of significant legal changes following a 2021 Spanish Supreme Court ruling that struck down the previous calculation method as unconstitutional in cases where the property had not actually increased in cadastral value. The current calculation methodology — introduced by Royal Decree-Law 26/2021 — gives sellers two options: the objective method (using official coefficients applied to the cadastral value) or the real gain method (applying the coefficient to the actual gain from the sale). Sellers can choose whichever method produces a lower tax bill. For most sellers in the current market, where prices have appreciated significantly, the objective method typically produces a lower plusvalía bill than the real gain method, but this should be verified case by case by the gestoria or lawyer handling the sale.

Making Sure Your IRNR Declarations Are Up to Date Before You Sell

Non-resident property owners in Mallorca are required to file an annual IRNR declaration (via Modelo 210) covering the imputed income from their Spanish property — typically 1.1 or 2 percent of the cadastral value per year, taxed at 19 or 24 percent depending on nationality. Many non-resident owners are unaware of this obligation, particularly those who purchased many years ago when the enforcement was less rigorous, or who have never rented the property and assumed no Spanish tax filing was required.

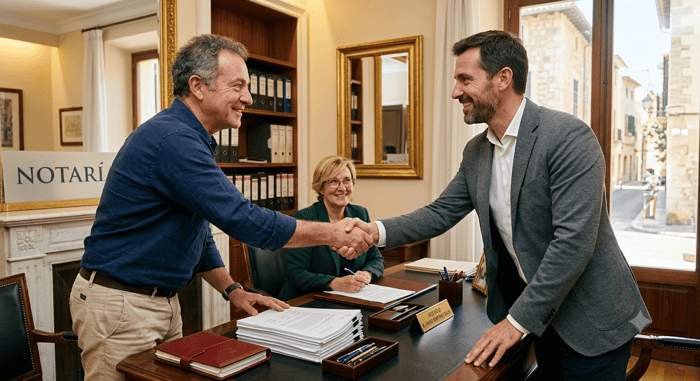

Before a property sale can proceed smoothly, the buyer's lawyer will typically request confirmation that the seller's Spanish tax obligations are up to date. Outstanding IRNR declarations create a complication at completion that is avoidable with some planning. If you have not filed IRNR declarations for some or all of the years you have owned your Mallorca property, the first step before putting the property on the market is to engage a Spanish tax adviser to regularise the position. The penalties for late filing are manageable when addressed proactively — they become more complex when discovered at the notary table.

The Energy Performance Certificate — A Legal Requirement Before Listing

Since 2013, a valid energy performance certificate (Certificado de Eficiencia Energética) has been a legal requirement for any property being sold in Spain. Without it, the property cannot be legally advertised for sale and the notary will not proceed to completion. The certificate must be issued by a qualified technician, is valid for 10 years and rates the property on a scale from A (most efficient) to G (least efficient). Most older Mallorcan villas without significant energy upgrades rate E or F. The certificate costs between 150 and 400 euros for a typical villa and takes a few days to obtain. It is one of those requirements that occasionally surprises sellers who have not sold a Spanish property before — mentioning it early in the process avoids a last-minute scramble.

The Full Cost of Selling — What Comes Out of the Sale Price

Non-resident sellers in Mallorca should plan for the following costs to be deducted from the gross sale proceeds:

Agent commission: typically 5 to 6 percent of the sale price in the Mallorcan market, though this varies by agency and property type. This is the single largest cost of selling and should be agreed in writing before the property goes on the market.

Capital gains tax: 19 percent of the net gain after deductible costs, as described above. The 3 percent retention covers part or all of this; any excess is refunded, any shortfall must be paid.

Plusvalía municipal: 3,000 to 15,000 euros for most southwest Mallorca properties depending on cadastral value and years of ownership.

Notary and legal fees: The seller's notary costs are relatively modest — typically 300 to 600 euros for the seller's portion. Lawyer and gestoria fees for the sale side run 1,000 to 3,000 euros depending on complexity.

Cancellation of existing mortgage: If the property is mortgaged, the mortgage must be cancelled at the same notary appointment and the redemption figure settled from the sale proceeds. The notary fees for the mortgage cancellation add 200 to 500 euros.

Energy performance certificate: 150 to 400 euros.

In total, the costs of selling a Mallorcan property as a non-resident — excluding capital gains tax, which depends on the gain — typically run between 6 and 8 percent of the gross sale price. On a 1 million euro sale with a meaningful capital gain, total deductions including CGT can run to 15 to 20 percent of the sale price. Modelling these costs accurately before agreeing a sale price is one of the most practical things a seller can do.

The Timeline — From Decision to Completion

For a non-resident selling in the current Mallorcan market, a realistic end-to-end timeline runs as follows. Preparation — obtaining the energy certificate, regularising any outstanding IRNR declarations, gathering purchase documentation and improvement invoices — takes two to four weeks. Listing and marketing — from going live to receiving a serious offer in the current market for a well-priced quality property — can be anywhere from a few weeks to several months depending on the property, price and market conditions. Offer to arras contract — once a buyer is identified and terms are agreed, the arras contract is typically signed within two to three weeks. Arras to completion — for a cash buyer, completion can follow in four to six weeks. For a buyer requiring a mortgage, the timeline extends to 12 to 16 weeks. After completion, the 3 percent retention refund process begins — expect 6 to 18 months for the AEAT to process the reclamation if one is due.

If you are considering selling your Mallorca property and would like to discuss the process or have your property valued, our team is happy to help.

Call or WhatsApp: +34 971 692 434 | Chat on WhatsApp

Email: help@imperial-properties.com

Read our guide to Spanish tax residency for Mallorca property owners

Read our guide to mortgages for non-residents in Mallorca