Table of Contents

Mallorca Property Market Report 2026 - Prices Trends and What the Data Shows

The Mallorca property market enters 2026 with a fundamental characteristic that has defined it for over a decade and shows no sign of changing: demand consistently exceeds supply, and the combination of protected land, strict planning constraints, strong international buyer interest and the island's genuinely finite coastline means that this structural imbalance is not going to be resolved by new development. The result is a market that grows in value across cycles, maintains liquidity at the upper end even when other European markets stall, and continues to attract the full international spectrum of buyers from northern Europe, North America and, increasingly, the Gulf states and other long-haul markets. This report sets out the key verified data points for the Mallorca property market in 2026: island-wide average prices, prices by zone, transaction volumes, foreign buyer composition, and the factors that independent analysis identifies as driving continued growth.

Island-Wide Average Prices in 2026

The headline figure for the Mallorca property market comes from the Steinbeis Transfer Institute's 2026 market study, which places the island-wide average at €7,370 per square metre, representing a year-on-year increase of 9.8 per cent. This figure applies to the market as a whole across all property types and locations; individual zones and the luxury segment perform considerably differently from this island average.

Independent portal data for April 2026 shows average asking prices in Palma de Mallorca city at €5,477 per square metre, an increase of 0.88 per cent compared to April 2025. Transaction-level estimates for Palma in early 2026 are calibrated at approximately €4,300 per square metre (the difference between asking and transaction prices reflecting the gap between listed and achieved figures). The Palma city market peaked in January 2026 at €5,585 per square metre asking price before stabilising.

The 10-year price growth picture is the most compelling data point for anyone assessing the Mallorca market as a long-term investment: prices have risen by approximately 97 per cent since 2015 in nominal terms, according to Fotocasa and Tasalia data. Over the last five years across the Balearics, prices per square metre have risen approximately 45 to 50 per cent. Over the last decade, the compound average growth has been approximately 7 per cent per year in nominal terms.

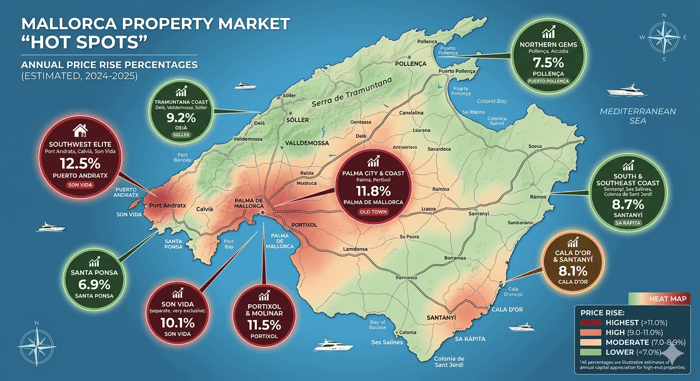

Prices by Zone - Where the Market Sits in 2026

| Zone | Price Range per m2 (2026) | Typical Property Types |

|---|---|---|

| Son Vida (Palma) | €7,000–€10,000+ | Luxury villas, gated estates |

| Port d'Andratx / Andratx | €7,500+ | Sea-view villas, luxury apartments |

| Deia / Soller (Tramuntana) | €6,000–€9,000 | Stone fincas, village houses |

| Bendinat / Portals Nous | €5,500–€8,000 | Villas, townhouses, apartments |

| Santa Ponsa / Calvià | €4,500–€7,500 | Villas, golf development properties |

| Old Town Palma / La Seu | €4,000–€6,993 | Renovated apartments, Can palaces |

| Santa Catalina (Palma) | €3,000–€4,500 | Renovated apartments, townhouses |

| Portixol / El Molinar (Palma) | €3,500–€5,000 | Waterfront apartments, houses |

| Pollensa / Puerto Pollensa | €4,000–€7,000 | Villas, village houses, apartments |

| Alcudia / Puerto Alcudia | €3,500–€5,500 | New builds, townhouses, villas |

| Santanyi / Cala d'Or (SE) | €4,000–€7,000 | Fincas, villas, village houses |

| Interior (Binissalem / Inca) | €2,000–€4,000 | Fincas, village houses, plots |

The premium segment — properties above €3 million in prime coastal and Son Vida locations — is the most liquid and most internationally driven part of the market. Prime sea-view properties with pools represent only around 2 per cent of total available stock on the island in 2026, according to the Steinbeis study. This extreme scarcity of the most sought-after product type is a structural driver of value at the top of the market that is unrelated to interest rate cycles.

Transaction Volumes and Market Activity

The Mallorca property market operates at a scale of approximately 10,500 annual transactions across the island, broadly consistent with the 10-year average. The market entered 2026 with stable transaction volumes and moderate price growth of 3 to 5 per cent expected across the island as a whole, with the luxury and premium segment outperforming at 5 to 8 per cent growth, according to independent analyst Reiderstad Invest's 2026 market forecast. The mid-range segment (properties below €1 million in the secondary market) shows more modest price movement, most sensitive to mortgage rates and cost-of-living conditions affecting domestic Spanish buyers.

New-build activity on the island increased by approximately 18 per cent in 2024, but strict planning rules, extensive areas of protected land (particularly the Serra de Tramuntana UNESCO World Heritage Site and the protected natural parks), and the prohibition on coastal development within the ZEPA and ZEPAL zones mean that new supply remains structurally constrained. The island cannot expand its premium coastal supply in any meaningful way, which is the fundamental underpinning of long-term value in the prime segment.

Foreign Buyer Composition in 2026

Foreign buyers account for approximately 30 to 33 per cent of all residential property transactions in the Balearic Islands in 2026, one of the highest proportions of any region in Spain. In the premium segment of the Mallorca market specifically, foreign buyer share is considerably higher: in the luxury villa market above €2 million, international buyers account for the majority of transactions.

The nationality composition of foreign buyers in the Mallorca premium segment in 2026 is as follows, according to data from Reiderstad Invest:

| Nationality | Share of Premium Segment |

|---|---|

| German | 58% |

| British | 10% |

| Spanish | 9% |

| Swedish / Scandinavian | 7% |

| Swiss | 5% |

| Other (US, Gulf, French) | 11% |

German buyers remain by far the dominant international force in Mallorca's premium property market, a position they have held for over 30 years and that is reinforced by the island's strong connections to German-speaking markets, the established German community and school infrastructure, and the cultural familiarity that comes from Mallorca being the single most visited Mediterranean island by German tourists. British buyers, despite the post-Brexit administrative layer, remain a significant and consistent second force in the market. American and Gulf state buyers are a growing category, supported by the establishment of new direct flight routes including the Etihad Abu Dhabi to Palma service launching June 2026 and the United Airlines Newark direct service.

Key Market Drivers in 2026

Several independently identified factors support continued growth in the Mallorca property market in 2026 and beyond. The Balearic Islands wealth tax threshold was raised in 2024 from €700,000 to €3 million per person, significantly reducing the tax burden on high-net-worth buyers and removing a deterrent that had been a friction point for larger purchases. The island continues to benefit from ongoing investment in Palma Airport, which is undergoing a €550 million expansion and serves 166 destinations across 52 airlines. The establishment of new long-haul routes from the Gulf and North America expands the universe of buyers who can access the island direct. The Balearic rental market continues to tighten as short-term rental licensing becomes more restricted, which supports values for properties with existing vacation rental licences.

Is Mallorca Property a Good Investment in 2026

The case for Mallorca property as a long-term investment rests on several independently verifiable structural factors. Supply is genuinely constrained by geography and planning: the island cannot grow its coastline and cannot significantly expand premium coastal supply. Demand is structural and international: it is not dependent on the domestic Spanish economy and it is not going to be replaced by an equivalent alternative location. The 10-year nominal price growth of 97 per cent demonstrates that the market has consistently delivered over a full cycle. The legal framework for ownership is clear, secure and well-understood. The lifestyle case — the reason buyers are attracted to the island in the first place — is not diminishing.

The risks that any honest assessment must acknowledge include liquidity risk at the lower end of the market (smaller apartments in non-prime areas can be slow to sell), regulatory risk around short-term rental income (licensing is tightening), and price-to-income sustainability risk for domestic buyers (though this affects a different segment than the international market). For international buyers in the premium segment, these risks are substantially offset by the structural factors described above.

At Imperial Properties, we provide buyers with independent, factual market data as part of our standard service and do not make speculative price forecasts. We are happy to discuss the current market in detail and to provide verified data on specific areas and property types. Contact us to arrange a conversation with one of our advisors.