Table of Contents

- Can Non-Residents Get a Spanish Mortgage?

- How Much Can You Borrow? The LTV Rules

- Interest Rates for Non-Residents in 2025 and 2026

- Affordability: The Debt-to-Income Rule

- Documents Required: The Complete List

- Which Banks Work Best with Non-Resident Buyers?

- The Step-by-Step Mortgage Process

- What Does the Mortgage Cost?

- Currency Risk: A Consideration for Non-Euro Buyers

- Working with Imperial Properties

Getting a Mortgage in Mallorca as a Non-Resident: What Banks Actually Require

The idea that buying property in Mallorca as a non-resident means paying entirely in cash is a common misconception. Spanish banks actively lend to foreign buyers, and the non-resident mortgage market is well established, well regulated, and accessible to buyers from across the European Union and beyond. The terms are different from those available to Spanish residents, and the documentation requirements are more detailed, but for a buyer with a stable income, a clean credit history, and a clear picture of what the process involves, securing a mortgage for a Mallorca property is a straightforward and manageable step. This guide explains everything you need to know, from what banks actually look for to the costs involved and the timeline from application to keys.

Can Non-Residents Get a Spanish Mortgage?

Yes, definitively. All of the major Spanish banks, including CaixaBank, Banco Santander, BBVA, Banco Sabadell, and Bankinter, offer mortgage products specifically designed for non-resident foreign buyers. According to the Colegio de Registradores, nearly 93,000 property purchases in Spain in 2024 were made by foreigners, representing approximately 15 percent of all transactions, and a meaningful proportion of those purchases were mortgage-financed. Non-residents from EU countries, the United Kingdom, the United States, Switzerland, Canada, and most other countries with stable currencies are eligible to apply.

The fundamental difference between a resident and a non-resident mortgage in Spain is not whether you can borrow, but how much, on what terms, and with what level of documentation. Understanding these differences clearly before you begin your property search in Mallorca puts you in the strongest possible position when the time comes to make an offer.

How Much Can You Borrow? The LTV Rules

The most important practical difference between resident and non-resident mortgages in Spain is the Loan-to-Value ratio, or LTV. This is the percentage of the property’s value that a bank will lend, with the remaining amount to be provided by the buyer as a deposit.

Spanish residents can typically borrow up to 80 percent of a property’s appraised value. Non-residents are generally capped at between 60 and 70 percent, depending on the lender, the buyer’s financial profile, and the nature of the property. For EU citizens or buyers with a particularly strong financial profile, some lenders will consider up to 70 or 75 percent. For buyers whose income is in a currency other than euros, some banks apply a slightly more conservative approach, typically around 60 percent, to account for foreign exchange risk.

What this means in practice is that as a non-resident buyer in Mallorca, you should plan to have a cash deposit of between 30 and 40 percent of the purchase price available, plus a further 10 to 14 percent to cover purchase taxes, notary fees, Land Registry costs, and legal fees. For a property at 500,000 euros, this means having between 200,000 and 270,000 euros available in cash before the mortgage complements the balance.

It is also important to understand that the bank will always lend against the lower of the purchase price and their own independent valuation (tasación). If the bank’s valuer assesses the property at less than the agreed purchase price, the LTV is calculated against the valuation figure, not the price. Any shortfall between the bank’s maximum lending and the purchase price must be covered from the buyer’s own funds.

Interest Rates for Non-Residents in 2025 and 2026

Spanish mortgage interest rates have followed the broader European trend, moving sharply upward in 2022 and 2023 and then falling progressively through 2024 and into 2025 as the European Central Bank reduced its key rate on multiple occasions. The 12-month Euribor, which underpins variable-rate mortgages in Spain, stood at approximately 2.27 percent in January 2026, well below its October 2023 peak of 4.2 percent.

For non-resident buyers, fixed-rate mortgages currently range between approximately 3 and 4.5 percent per annum, depending on the lender, the loan term, the LTV, and the individual financial profile of the applicant. Variable-rate mortgages are priced at Euribor plus a bank margin, which typically ranges from 0.5 to 2 percent. Non-residents generally pay a premium of between 0.3 and 0.7 percent above the rates available to residents, reflecting the additional risk assessment that banks apply to overseas borrowers.

Fixed-rate mortgages have become the preferred choice for most non-resident buyers in Mallorca, primarily because they provide payment certainty in a currency that for many buyers is not their domestic one. A fixed rate eliminates the risk of monthly payments increasing with Euribor movements, which is a meaningful advantage for buyers managing income in sterling, US dollars, or other non-euro currencies.

Mortgage terms for non-residents are generally capped at between 20 and 25 years, compared to up to 30 or even 40 years for Spanish residents. Most lenders also apply a maximum age at the end of the mortgage term, typically between 70 and 75 years.

Affordability: The Debt-to-Income Rule

Spanish banks apply a strict affordability test. The total of all monthly debt repayments, including the proposed Spanish mortgage and any existing loan obligations in the applicant’s home country, must not exceed 30 to 35 percent of verified net monthly income. This is a firm limit, and banks apply it consistently regardless of the apparent overall wealth of the applicant.

Income must be verified and stable. Employed applicants are assessed on the basis of their employment contracts and recent payslips. Self-employed applicants are assessed on the basis of tax returns, typically for the most recent two to three years, with lenders looking for consistent and demonstrable income over that period rather than a single strong year. Income received in a foreign currency is assessed at the current exchange rate, with some banks applying a small buffer to account for fluctuation.

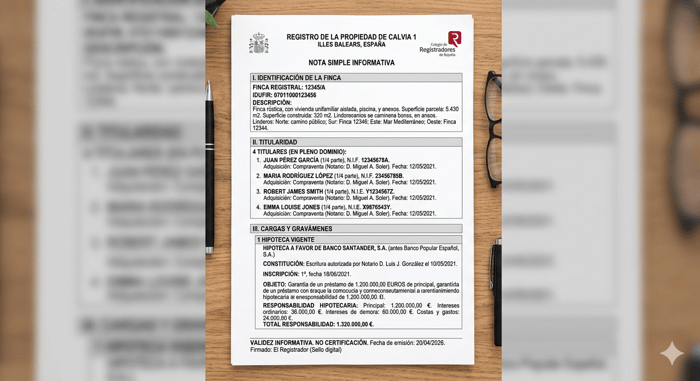

Documents Required: The Complete List

The documentation required for a non-resident mortgage application in Spain is more extensive than many buyers expect, and all documents not originally in Spanish must be officially translated by a sworn translator (traductor jurado). For buyers from countries outside the EU, some documents may additionally require an apostille certification to be accepted.

The standard document set includes: a valid passport, your NIE, proof of address in your country of residence, your last two to three years’ personal tax returns, your last three to six months’ payslips or self-employment accounts, bank statements for the last three to six months, a credit report from your country of residence, details of any existing mortgages or financial commitments, and the Nota Simple and purchase contract for the property you are buying. American buyers must also provide FATCA documentation including Form W-9 and IRS tax transcripts.

Which Banks Work Best with Non-Resident Buyers?

CaixaBank’s HolaBank service is specifically designed for international clients, accepts documents in their original language for initial pre-approval, and issues a viability assessment within 72 hours. Banco Santander publishes dedicated non-resident mortgage products with English-language support. BBVA offers a fully digital application process with a mortgage calculator available in English. Banco Sabadell operates English, French, and German-language service lines for non-resident mortgage enquiries.

Many buyers in Mallorca find that working with an independent mortgage broker who specialises in non-resident Spanish mortgages produces better results than approaching a single bank directly. A specialist broker can submit applications to multiple lenders simultaneously, compare offers, and negotiate on margins and arrangement fees in a way that individual buyers rarely have the leverage to achieve.

The Step-by-Step Mortgage Process

The process begins with a pre-assessment — submitting basic financial information to a bank or broker for an indicative assessment of borrowing capacity. Once a property is identified, a contrato de arras is signed and a deposit of approximately 10 percent of the purchase price is paid, triggering the formal application. The bank then commissions an independent valuation (tasación), costing between 300 and 600 euros, paid by the buyer. The bank issues its formal binding offer (oferta vinculante), which under the 2019 Mortgage Law must be provided at least ten days before signing. An acta de transparencia meeting with a notary, required at least one business day before signing, independently confirms the buyer understands all key mortgage terms. Finally, the purchase deed and mortgage deed are signed simultaneously at the notary. The total timeline from full document submission to signing is typically six to ten weeks.

What Does the Mortgage Cost?

The 2019 Spanish Mortgage Law significantly improved the cost position for borrowers by shifting several fees to the lender. Under current rules, the bank pays the notary fees for the mortgage deed, the Land Registry inscription costs, the stamp duty on the mortgage document (AJD), and the gestoria costs. The buyer pays the property valuation fee and the bank’s arrangement fee if charged, typically around 1 percent of the loan amount. All purchase costs — ITP on resale properties, VAT and AJD on new builds, notary, registry, and legal fees — total between 10 and 14 percent of the purchase price and must be funded entirely from the buyer’s own cash.

Currency Risk: A Consideration for Non-Euro Buyers

For buyers whose income is in sterling, US dollars, or another non-euro currency, a euro-denominated mortgage creates ongoing currency exposure. If the euro strengthens against your home currency, your monthly mortgage payments become more expensive in real terms. Many non-resident property owners in Mallorca hold a euro reserve account or arrange a regular currency conversion to cover mortgage payments at a pre-agreed rate. Specialist currency exchange services are widely used by international property owners for this purpose.

Working with Imperial Properties

At Imperial Properties, we work with buyers at every stage of the financing process, from helping you understand what you are likely to be able to borrow before you begin your search, to connecting you with specialist mortgage brokers and independent lawyers with extensive experience in non-resident purchases across Mallorca. Visit www.imperial-properties.com or contact our team directly to get started.